South Africa’s SMME sector is widely recognised as a powerful engine for inclusive growth, job creation, and entrepreneurship. Yet, for many small, micro, and medium enterprises (SMMEs), growth is constrained by a persistent structural challenge: access to finance.

This is part of a much larger global trend.

The Alliance for Financial Inclusion estimates that the global financing gap for formal SMMEs stands at $5.7 trillion. In Africa, the gap is approximately $331 billion, while South Africa’s shortfall is estimated at between R350 billion and R386 billion. This is despite the country having a relatively advanced financial system and strong levels of private sector credit.

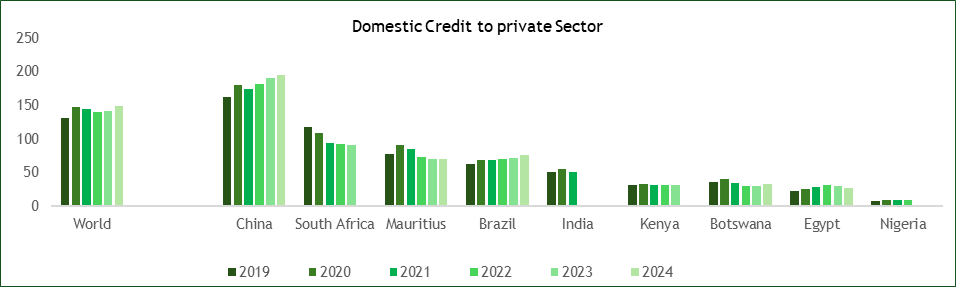

Source: World Bank Data – A high credit to the private sector tends to indicate strong financial intermediation, capital formation, high entrepreneurial activity, and solid economic output. South Africa’s Domestic credit to the private sector is considerably higher than that of other developing markets.

Why Tourism Businesses Are Locked Out of Funding

For tourism SMMEs, accessing finance is especially challenging. Traditional lenders often view smaller businesses as high-risk, particularly in their early stages. Additionally, the more innovative the business model, the greater the perceived risk-return profile. Many lack collateral, credit history, or audited financial records, all of which are typically needed to secure funding.

The nature of tourism businesses adds another layer of complexity. Much of their value lies in intangible assets, such as experiences, brand, and location, rather than in physical assets that can be used as collateral. Following the 2008 global financial crisis, lending regulations have become more stringent, with financial institutions placing greater emphasis on risk mitigation. While necessary for financial stability, these regulations have also made it harder for small businesses to access credit, with banks often prioritizing large enterprises.

Why This Matters for South Africa’s Economy

The inability of MSMEs to access finance has significant consequences. According to the World Bank, SMMEs contribute around 40% of GDP in developing economies and represent up to 90% of businesses worldwide. In Africa, SMEs are responsible for roughly 80% of jobs, and in South Africa, they comprise about 90% of formal enterprises, while SMEs in the tourism sector contribute approximately 39% of the economy, with over 1 million MSMEs.

Tourism plays a particularly important role in South Africa; the government has identified it as a priority sector because of its inclusivity and multiplier effect. It is an inclusive sector and is deeply interconnected with other sectors, from transport to agriculture. A strong tourism SMME base not only creates jobs but also distributes economic benefits across communities.

New Financing Models Are Starting to Shift the Landscape

Reassuringly, governments and development finance institutions tend to act as catalytic agents by introducing loan guarantees to encourage private sector lending. One such risk-sharing agreement is the partnership between the African Development Bank and the Standard Bank Group. The collaboration includes a R3.6 billion social bond and a $200 million risk participation agreement. These risk-sharing instruments allow banks to expand lending to SMMEs while reducing the risk exposure of lending institutions.

Institutions such as the African Guarantee Fund play a similar role by providing guarantees to financial institutions. Local banks like Nedbank are increasingly offering tailored solutions designed specifically for small businesses.

Further, there is a broader ecosystem of support for MSMEs. Government and private sector initiatives, such as the Tourism Incentive Programme by the National Department of Tourism (NDT), are helping to unlock funding for sector growth.

The programmes offered by the NDT include;

- The Green Tourism Incentive Programme,

- Tourism Transformation Fund

- Tourism Equity Fund

- Market Access Support Programme

- Tourism Grading Support Programme

- SMME connectors; Provincial Organisations such as the Gauteng Tourism Authority also play a vital role in connecting SMMEs to key buyers through South African Tourism-owned assets, affording these SMMEs market access to sell their tourism products to International buyers, as well as providing training to these SMMEs.

- City Lodge Hotels (CLH), in collaboration with Sigma International and the SATSA Tourism Business Incubator providing business development support

- National Youth Development Agency (NYDA) grants (South Africa): The NYDA offers grant funding for youth entrepreneurship and co-operatives.

- Coega SEZ bridge financing scheme (South Africa): This scheme supports local MSMEs that provide services and construction work for the Coega Special Economic Zone.

- Financial Sector Charter and BBBEE (South Africa): These initiatives aim to promote Broad-Based Black Economic Empowerment and to expand access to finance for previously disadvantaged individuals.

- Khula Enterprise Finance Limited offers financing and support to SMEs.

- The South African microfinance company, Apex Fund, supports micro and small enterprises.

- African Women’s Development Fund (AWDF): provides grants to women-owned businesses in Africa, including Arara, Banco.

- Asante Financial Services.

Closing the Gap Requires More Than Just Funding

While the goal is to see significant improvement on the supply side, access to finance remains limited by a lack of awareness of available programs and instruments for MSMEs, as well as by financial readiness among SMMEs. Many businesses do not know about the funding options or lack the financial literacy needed to qualify. Skills such as keeping financial records, understanding cash flow, and demonstrating creditworthiness continue to pose barriers for MSMEs.

Evidence from OECD countries shows that while traditional bank lending to small businesses is declining, alternative financing models are gaining popularity. This creates an opportunity for South Africa to further diversify its funding options and better meet the needs of sectors like tourism.

Ultimately, unlocking finance for tourism SMMEs is about more than just enabling business growth. It is about supporting a sector with the potential to promote large-scale inclusive economic development. With the right combination of innovation, policy support, and financial education, South Africa can start to bridge the gap and realize the potential of its tourism economy.